A 529 plan account owner may change the beneficiary at any time without tax consequences when the new beneficiary is a family member of the current beneficiary. The IRS provides a broad definition of family member, which includes the beneficiary’s blood relatives and relatives by marriage and adoption.

It’s important to understand who qualifies as a member of the beneficiary’s family before you change your 529 plan beneficiary.

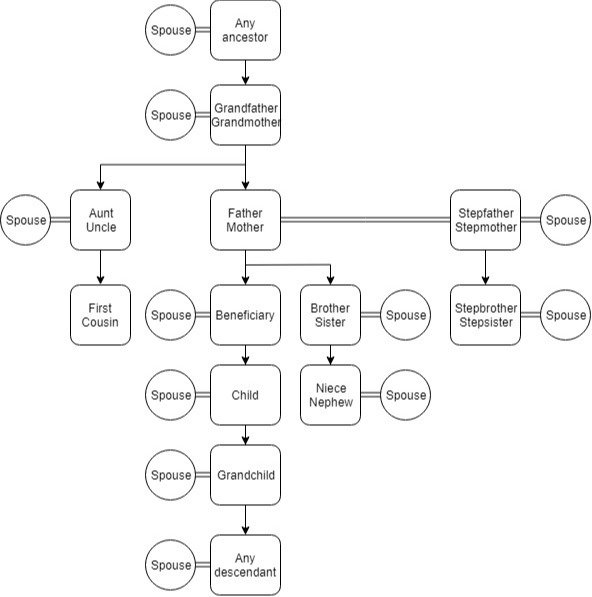

Who is a member of the family?

According to the IRS, a member of a 529 plan beneficiary’s family includes the beneficiary’s:

- Spouse

- Son, daughter, stepchild, foster child, adopted child or a descendant

- Son-in-law, daughter-in-law

- Siblings or step-siblings

- Brother-in-law, sister-in-law

- Father-in-law, mother-in-law

- Father or mother or ancestor of either, stepmother, stepfather

- Aunt, uncle or their spouse

- Niece, nephew or their spouse

- First cousin or their spouse

A 529 plan beneficiary could also be changed to an ancestor of a stepfather or stepmother, even though they are not listed. To make this change, the 529 plan account owner would change the beneficiary to the stepfather or stepmother and then subsequently change the beneficiary to be their mother or father or any ancestor (assuming they are still living).

It is still possible to help friends and other non-family members pay for college. 529 plans accept gift contributions from any third party, regardless of whether the gift giver is a member of the family.

529 plan beneficiary – Member of the family

Changing a 529 plan beneficiary

529 plans are designed to save for future education expenses for a single designated beneficiary. However, a 529 plan account owner may change the beneficiary by completing a form on the 529 plan’s website. Beneficiary changes are not treated as a distribution when the new beneficiary is a member of the family of the current beneficiary.

There are several reasons why a 529 plan account owner may want to change the beneficiary. For example, tax-free 529 plan distributions may be used to pay for qualified education expenses for one child only. Families who use a single 529 plan to save for more than one child’s college will have to change the beneficiary once they are ready to pay for the next sibling’s college expenses.

Distributions used to pay for college expenses for anyone other than the designated beneficiary will be considered non-qualified, and subject to income tax and a 10% penalty on the earnings portion and possible recapture of state income tax benefits.

Families may also be able to avoid the twice per calendar limit on 529 plan investment changes and the one rollover per 12-month period limitations when the request is submitted with a beneficiary change request.

Generation-skipping transfer tax

Changing a 529 plan beneficiary may result in generation-skipping transfer tax (GST) when the new beneficiary is two or more generations below the current beneficiary. For example, when a 529 plan beneficiary is changed from a grandparent to a grandchild the grandparent’s estate would be subject to the GST. A grandparent may have been named a 529 plan beneficiary if they opened a 529 plan account before the grandchild was born.

However, the majority of families will not have to pay taxes when changing a 529 plan beneficiary from a grandparent to a grandchild. Up to $15,000 per year ($30,000 if married) qualifies for the annual GST exclusion, and up to $11,180,000 per individual qualifies for the lifetime gift tax exemption. Under federal law, 529 plan balances cannot exceed the expected cost of the beneficiary’s higher education expenses, and state aggregate 529 plan balances range from $235,000 to $529,000.

The GST may also apply when grandparents contribute to a grandchild’s 529 plan. A grandparent may shelter up to $75,000 from estate taxes in a given year if they elect to treat the contribution as if it were made over a 5-year period. With 5-year gift tax averaging, each grandparent can gift up to $75,000 per grandchild.