In this article

- The Gerber Life College Plan annual earnings are as low as 1.76%

- The Gerber Life College Plan performance is similar to short-term bank CDs

- 5-year bank CDs and 529 plans beat the Gerber Life College Plan

- The Gerber Life College Plan hurts eligibility for need-based financial aid

The Gerber Life College Plan by Gerber Life Insurance promises guaranteed growth and the flexibility to use the money to pay for college or other expenses. But, the investment earnings are taxable and do not keep pace with college tuition inflation. The Gerber Life College Plan also offers inferior performance as compared with the return on investment available on FDIC-insured Certificates of Deposit and 529 college savings plans.

Gerber Life College Plan yields low earnings

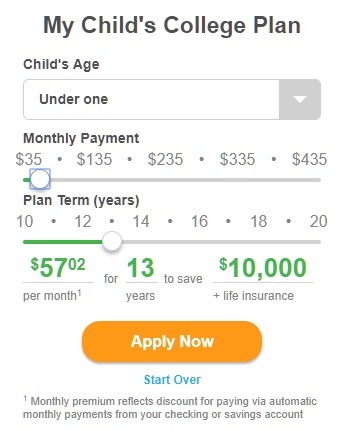

The My Child’s College Plan tool on the Gerber Life Insurance web site calculates the total savings for various monthly payment amounts and plan terms in years. For example, this snapshot shows that payments of $57.02 per month for 13 years yield a total of $10,000 in savings or plan payout.

That’s the equivalent of an annualized return on investment of 1.76%.

Other examples yield higher interest rates, which seem to center around about 2.6% to 2.7% annual ROI, though a few apparent edge cases yield a lower annual ROI.

- $42.50 per month for 16 years yields $10,000, the equivalent of a 2.46% annual ROI

- $51.72 per month for 14 years yields $10,000, the equivalent of a 1.96% annual ROI

- $72.92 per month for 10 years yields $10,000, the equivalent of a 2.60% annual ROI

- $435.05 per month for 17 years yields $113,000, the equivalent of a 2.73% annual ROI

Note that these performance figures are before taxes. Families must pay taxes annually on the earnings from a Gerber Life College Plan, unlike a 529 college savings plan.

If a family cancels the Gerber Life College Plan, the refund value may be less than or equal to just the contributions made by the family. The plan payout is guaranteed only when the policy reaches maturity, if all plan premiums have been paid.

Gerber Life College Plan falls short of tuition inflation

The performance of the Gerber Life College Plan does not keep pace with college tuition inflation. Current tuition inflation is 3.6 percent at private 4-year colleges and 3.1 percent at in-state public 4-year colleges, according to the College Board’s Trends in College Pricing 2017.

Longer-term tuition inflation is even higher. Using a 17-year moving average, tuition inflation averaged 4.6 percent at private 4-year colleges and 6.3 percent at in-state public 4-year colleges.

Gerber Life College Plan performance similar to short-term bank CDs

The performance of the Gerber Life College Plan is similar to the interest rates on current 1-year bank CDs, as reported by Bankrate.com.

The Gerber Life College Plan does lock in the earnings over a 10 to 20 year term. But, in a rising interest rate environment, one would expect a higher return on investment for a long-term investment. For example, the best interest rates on 5-year CDs, as reported by Bankrate.com, provide a higher return on investment than the Gerber Life College Plan.

Bank CDs also provide the benefit of FDIC insurance, which the Gerber Life College Plan does not.

529 College Savings Plans outperform Gerber Life College Plan

The performance of the Gerber Life College Plan is about half the current average return on investment of 529 college savings plans, as reported in Savingforcollege.com’s quarterly performance rankings. A 529 plan currently yields more than double the earnings of the Gerber Life College Plan.

529 plans also offer several tax advantages that aren’t available to the Gerber Life College Plan. The earnings in a 529 plan grow on a tax-deferred basis and are entirely tax-free when used to pay for qualified higher education expenses. More than two-thirds of states offer income tax deductions or credits for contributions to their 529 plan.

Gerber Life College Plan hurts financial aid eligibility

The Gerber Life College Plan appears to be a form of life insurance, which is not reported as an asset on the Free Application for Federal Student Aid (FAFSA). However, the full plan payout amount may need to be reported as income on the FAFSA, reducing eligibility for need-based financial aid by as much as half of the distribution amount.

Comparison of Gerber Life College Plan with CDs and 529 Plans

|

Gerber Life |

Long-term |

529 plans |

Interest rate |

2.7% |

3.25% |

6.0% |

Payout on $50.05/month at 17 years |

$13,000 |

$13,644 |

$17,768 |

Total earnings |

$2,790 |

$3,434 |

$7,558 |

Total taxes (24% Bracket) |

($670) |

($824) |

None |

Impact on financial aid |

($6,500) |

($102) |

None |

Total net of taxes and financial aid |

$5,830 |

$12,718 |

$17,768 |

Earnings net of taxes |

$2,120 |

$2,610 |

$7,558 |

Earnings net of taxes and financial aid |

($4,380) |

$2,508 |

$7,558 |