{{parent.cta_data.text}}

{{parent.title}}

{{parent.title}}

Login

Login

Do 529 plans beat their benchmark?

http://www.savingforcollege.com/articles/do-529-plans-beat-their-benchmark

Posted: 2014-05-02

Joe Hurley, Founder of Savingforcollege.com believes 529 plans are �The Best Way to Save for College� (he even wrote a whole book about it). But many people continue to worry that these plans are costly and not as well managed as other investment options. Until now, it�s been hard to measure just how well 529 plans are performing. However, a recent analysis conducted by Hurley found that historically when their unique benefits were taken into account, 529 plans were in fact a very lucrative choice when saving for college.

The top seven benefits of 529 plans

Similar to a retirement account such as an IRA, 529 plans offer federal tax-free growth on earnings. Additionally, the withdrawals will avoid federal tax if they are used toward qualified education expenses. Some 529 plans also offer additional state income tax savings for residents. If you are in a high tax bracket, this can add up to substantial savings.

But is the value of these tax benefits enough to justify investing in a 529 plan instead of a more traditional option?

How to make the most of your college savings

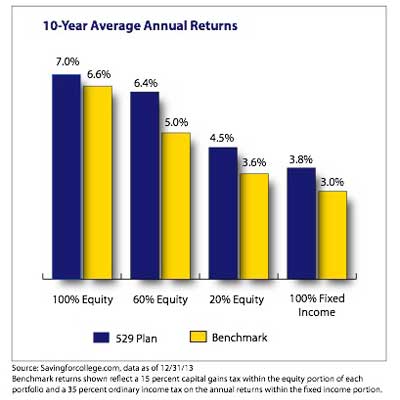

To answer this question, Hurley conducted a study comparing the average investment performance (net of fees) of 529 plans versus industry benchmarks over the same periods. At first glance, the 529 plans underperformed the benchmarks in almost every category. However, to illustrate the potential tax benefits of a 529 plan, Hurley adjusted the benchmark returns to reflect a 15 percent capital gains tax within the equity portion of each portfolio and a 35 percent ordinary income tax on the annual returns within the fixed income portion. This time, the results favored 529 plans.

On an after-tax basis, 529 plans beat the benchmark in every asset-allocation category and over every time period that generated positive returns. For example, if a saver had contributed $20,000 to a 529 plan 10 years ago, with the funds invested in the 60% equity portfolio, they would have an account balance of around $37,000 today. However, the same investment in the benchmark portfolio would have only ended up with about $33,000, after taxes. The chart below illustrates the 10-year average after-tax annual returns of 529 plans in different asset allocation categories and their respective benchmarks (as of 12/31/13).

While there are many investment alternatives available to you, 529 plans offer excellent growth potential for those saving for college.

See the full analysis here: Benching the 529 Industry

Joe Hurley, Founder of Savingforcollege.com believes 529 plans are �The Best Way to Save for College� (he even wrote a whole book about it). But many people continue to worry that these plans are costly and not as well managed as other investment options. Until now, it�s been hard to measure just how well 529 plans are performing. However, a recent analysis conducted by Hurley found that historically when their unique benefits were taken into account, 529 plans were in fact a very lucrative choice when saving for college.

The top seven benefits of 529 plans

Similar to a retirement account such as an IRA, 529 plans offer federal tax-free growth on earnings. Additionally, the withdrawals will avoid federal tax if they are used toward qualified education expenses. Some 529 plans also offer additional state income tax savings for residents. If you are in a high tax bracket, this can add up to substantial savings.

But is the value of these tax benefits enough to justify investing in a 529 plan instead of a more traditional option?

How to make the most of your college savings

To answer this question, Hurley conducted a study comparing the average investment performance (net of fees) of 529 plans versus industry benchmarks over the same periods. At first glance, the 529 plans underperformed the benchmarks in almost every category. However, to illustrate the potential tax benefits of a 529 plan, Hurley adjusted the benchmark returns to reflect a 15 percent capital gains tax within the equity portion of each portfolio and a 35 percent ordinary income tax on the annual returns within the fixed income portion. This time, the results favored 529 plans.

On an after-tax basis, 529 plans beat the benchmark in every asset-allocation category and over every time period that generated positive returns. For example, if a saver had contributed $20,000 to a 529 plan 10 years ago, with the funds invested in the 60% equity portfolio, they would have an account balance of around $37,000 today. However, the same investment in the benchmark portfolio would have only ended up with about $33,000, after taxes. The chart below illustrates the 10-year average after-tax annual returns of 529 plans in different asset allocation categories and their respective benchmarks (as of 12/31/13).

While there are many investment alternatives available to you, 529 plans offer excellent growth potential for those saving for college.

See the full analysis here: Benching the 529 Industry

Recommended Articles

SPONSOR CONTENT