{{parent.title}}

{{parent.title}}

Login

Login

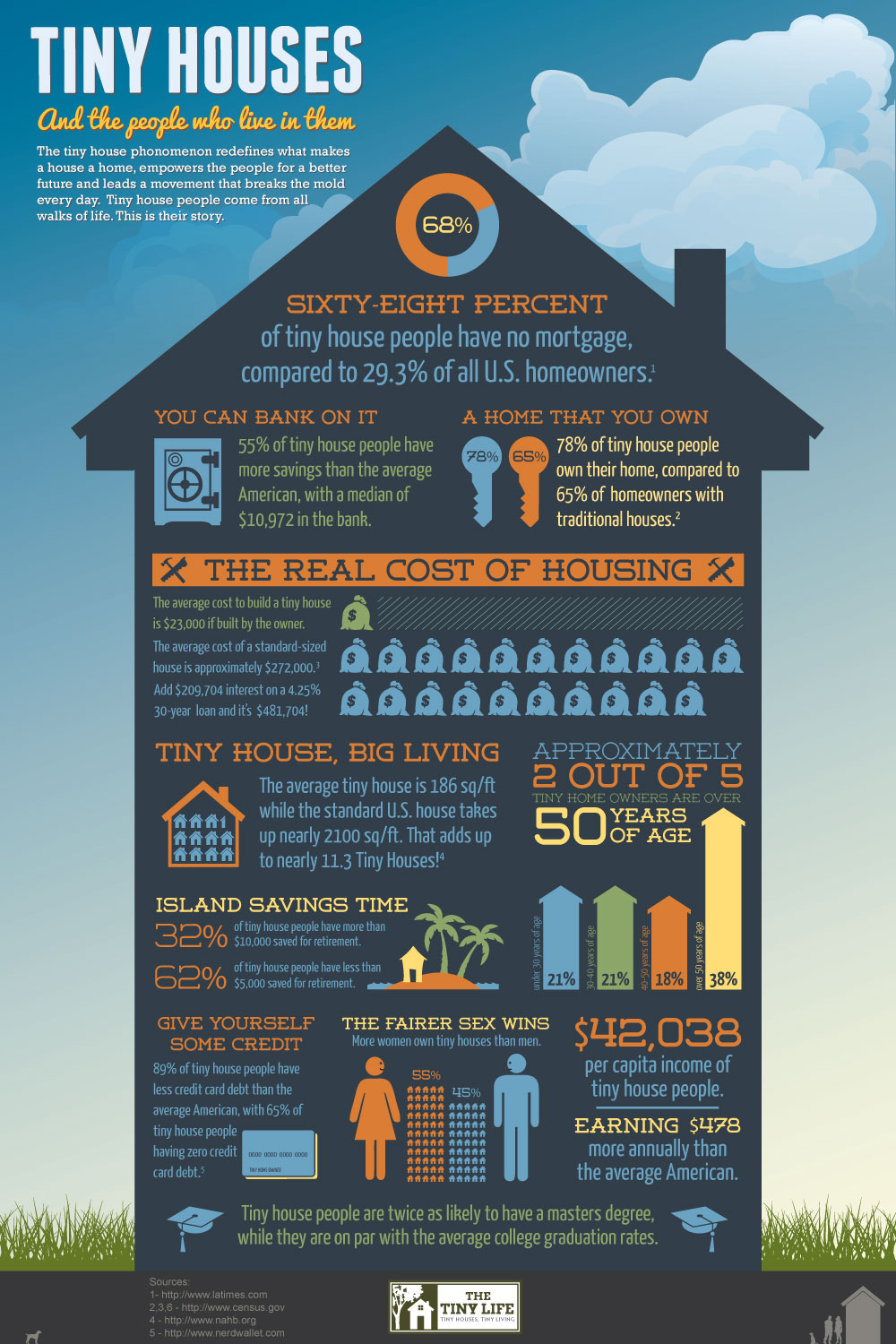

When Claudia Pennington graduated with her master’s degree, she had over $36,000 in student loan debt.

At first, she struggled to find a full-time job. She deferred her payments, then paid only the minimum, as she and her husband balanced her loan payments with their living expenses, including their home mortgage.

“We had a lot more house than we needed,” she said. “It was more space and more mortgage than we needed or wanted.”

They decided to downsize, selling their home and embracing the tiny house movement. Thanks to that switch, they reduced their expenses and were able to pay off their credit card and student loan debt in just four years.

“Before downsizing, our mortgage was $1,250 per month,” Pennington explained. “so by selling that [the house] and then moving into a smaller house, we were able to get a much smaller mortgage, and our bills were lower overall. So the extra money we knew we would be able to put toward our debt.”

Pennington is part of a growing trend of people deciding to live in tiny houses — homes that are generally 600 square feet or smaller — so they can accelerate their debt repayment. It might seem like a drastic step, but it can be incredibly effective.

5 ways a tiny home can help you manage your student loans

If you’re thinking about ways to pay off your student loans faster, here are five reasons why moving into a tiny home may be the solution:

1. It’s cheaper than the typical rental or mortgage payment.

Besides your student loans, your rent or mortgage payment is likely your biggest expense. Abodo reported that the national median rent for a one-bedroom apartment is $1,025.

Downsizing to a tiny home can dramatically reduce your housing expenses. According to The Tiny Life, the average cost to build a tiny home yourself is $23,000. If you financed the supplies with a five-year personal loan at 7% interest — a typical rate if you have good to excellent credit — your monthly payment would be just $455 per month.

If you went from the typical one-bedroom to a tiny house, that means you’d free up an extra $570 each month to pay off your loans. And, once the five-year term was over, you’d own your tiny home outright and have no payments at all.

2. Going tiny can reduce your utility bills.

As Pennington found out, going tiny doesn’t just reduce your monthly housing payment; it also reduces your utility bills.

According to the United States Department of Commerce, the average home in the United States is 2,687 square feet in size. All that space can be expensive to cool and heat. In fact, the typical monthly electric bill is $117.65 per month.

By cutting down your home’s size by 80% or more, you can similarly reduce your utility bill. That decrease can allow you to pay more towards your student loans each month.

3. Decluttering can help you earn extra money.

The average person has lots of unused stuff in their homes. Whether it’s toys, books, sports equipment, or old electronics, there’s a lot of clutter just gathering dust.

In a tiny home, there’s no room for unnecessary things, so it forces you to declutter. If you sell your unused items for cash, you could earn thousands to make a lump sum payment on your debt.

4. Tiny homes are more portable.

When you rent, your mobility is limited. If you find a better-paying job in another state, you’ll need to spend thousands to break your lease to move, or you may be on the hook for the remainder of your term.

By contrast, tiny homes can be more portable. Many of them are built on wheels or are renovated vans or campers, so you can simply drive to your new location and take advantage of opportunities.

5. There’s no room for extra stuff.

It’s easy to fritter your money away on extra purchases. Whether its new holiday decor, books, or toys for your kids, spending your hard-earned cash on those little expenditures can cause you to waste money.

When living in a tiny home, space is at a premium. It forces you to adopt a minimalist lifestyle, so you cut back on unnecessary spending. Over time, these small changes can speed up your loan repayment.

Moving into a tiny home

Transitioning into a tiny house isn’t for everyone. But if you’re overwhelmed with your debt, creative solutions like downsizing can help reduce your living expenses to free up extra money to pay down your student loan balances. Over time, the savings can be significant, and it can help you become debt-free years earlier.

Use the loan prepayment calculator to find out how much you can save by downsizing your lifestyle. If tiny homes aren’t for you, you can also consider refinancing student loans for a lower interest rate and lower monthly payment. Keep in mind refinancing federal student loans means a loss in many benefits – income-driven repayment, any federal forgiveness programs, generous deferment options, and more.

{kind=link}